Digital Lenders: Pros, Cons and How to Protect Yourself

Fintech has brought with it a wave of change in the financial industry, including digital lenders. These are lenders who give borrowers access to quick funds through mobile applications and digital lending platforms.

As regulators try to catch up with technology, unauthorized and predatory lenders have cropped up. But this doesn’t matter to many borrowers as long as you can get quick access to cash when you need it.

So, for today, let’s look at digital lenders and why they are probably not a good option for you.

Pros of Digital Lenders

There’s no denying that digital lenders have their advantages, including:

1. Ease of Access

With a click of a few buttons on your smartphone, tablet, or computer, you can get a loan from digital lenders. Regardless of who you are or where you are. Many traditional banks don’t even have any presence in remote areas of the country, while anyone with a mobile phone and network can access digital lenders.

Plus, you don’t even have to wait for a whole week to get the money. Most of these digital lenders will avail of the loan in a few hours or even minutes.

With traditional banks, you have to jump through hoops even to access a few thousand shillings. It’s even worse if you try applying for a loan and don’t have a steady income, like a paycheck. And, you have to wait a few business days before the money is deposited into your account.

2. Minimal Requirements

Have you applied for any digital loans? What were you required to provide? When I used to borrow from lenders like Mshwari, all I needed was a mobile phone and a Mpesa line. Then, the more you borrowed and paid diligently, the more your borrowing limit increased. Plus, you don’t have to visit any physical store for all of this.

With banks, you have to provide all sorts of documents and avail yourself in a brick-and-mortar shop to meet with relationship managers. For instance, you have to prove that you have a source of income and fill out endless forms.

Cons of Digital Loans

Now, that’s just about where the advantages of digital loans end. But, unfortunately, these are so persuasive enough that many people have become reliant on digital lenders for their day-to-day expenses and emergency bills.

There’s also no denying that there are high unemployment rates and low earnings with people living from paycheck to paycheck. This, combined with the above pros, makes mobile loans and other digital loans an easy option.

But it comes at a cost of predatory lending practices, including:

1. High-Interest Rates

Due to the lack of due diligence, mobile and digital lenders charge a hefty interest. These interests are so high, with some hitting an annual rate of 100%+! That’s way more than traditional banks are allowed by regulators to charge.

In the end, you accumulate more debt or pay digital lenders too much money in return for quick access to their loans.

2. High Fees

It’s not just the interest rates that are high. Other fees, like registration fees, loan processing fees, and late payment fees, drive the cost of digital and other mobile loans to the roof.

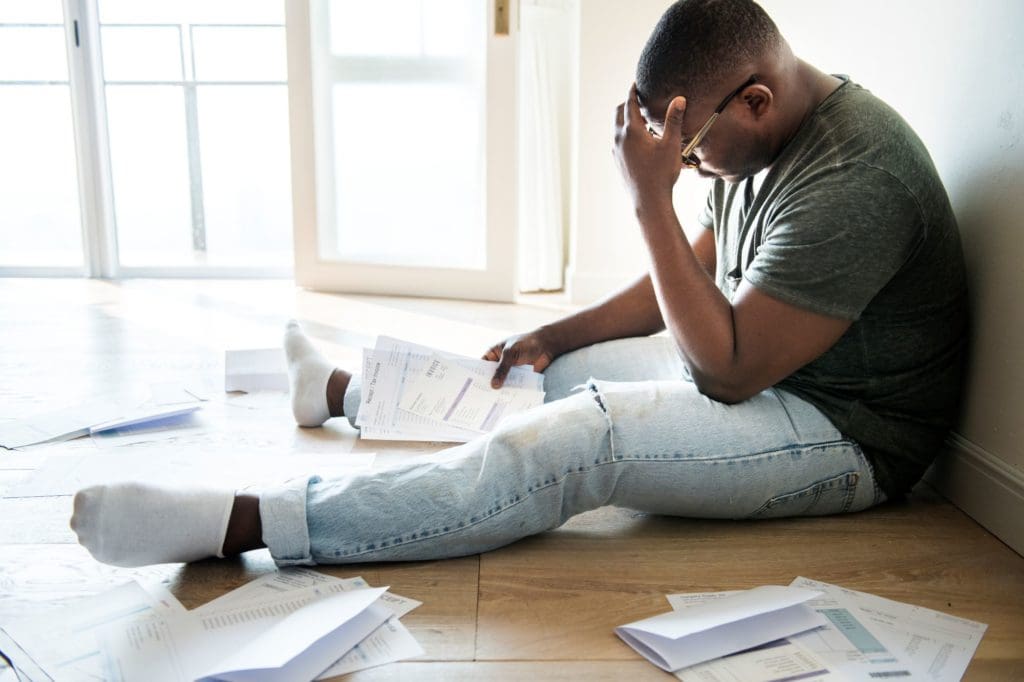

3. Harassment

Some of the lenders are harassing borrowers for failing to repay their loans. Even if you miss the payment by a single day or a few shillings, there’s the possibility of debt collectors harassing you.

4. No Privacy

It has become so bad; that they are even going after one’s contact list. Have you heard of people receiving threatening messages and calls from digital lenders for loans they never took? You end up putting people in your life in awkward positions dealing with debt collectors.

So, there you are, enjoying your day sipping your cup of tea, and you start getting threatening messages from unknown numbers for loans you never took. Why? Because someone had you on their contact list and the digital lender had access to it when they consented to their terms and conditions. Now, you have to deal with their harassment, endless messages and phone calls, and abusive language.

5. High Stress Levels

The harassment, high interest and fees, and the lack of privacy that leads to shaming have led to high stress levels among borrowers. Sadly, this has had worse results, with some borrowers committing suicide. And this is not just in Kenya.

How to Protect Yourself

While regulators are working to ensure regulation for mobile and other digital lenders, there’s no denying that we probably have a long way to go before there’s order in this space. So, here’s how you can start protecting yourself:

1. Start Managing Your Debts

I mentioned earlier that I used to get funds from these mobile lenders. That was a few years ago. And now that I think about it, I rarely used that money myself. I was mostly helping out a loved one because they had an emergency, and I didn’t have enough funds at my disposal to help them out.

The last straw was when I needed some quick funds myself. When I tried borrowing from one of the mobile lenders, I got a message that I was blacklisted. One of my lines was used to get a loan, which I had approved, by the way. But the loan was still outstanding. I really never paid too much attention because I thought the borrower was responsible enough to keep up with the payments.

That evening was an eye-opener for me. I swore to stop relying on mobile lenders and other loans. It was also the moment I started managing my relationships with loved ones regarding loans and money issues. I started working on a plan to pay any remaining mobile loans, my student loan, and some loans I had taken from a Sacco for my school expenses.

When I write posts about managing debts and trying to be debt-free, know that it’s possible. Of course, it will take time, especially if your income alone is not enough to meet your daily needs. But it’s doable.

Related read: Are You Too Deep In Debt? 5 Top Signs To Watch

2. Read the Terms and Conditions

Many borrowers never do this. Instead, you just tick the terms and conditions box to get moving and get the money ASAP. But, have you thought about the consequences? The terms and conditions you agree to are the contract between you and the lender. So, by default, they have the right to do whatever they want because you agree to their conditions.

3. Manage the App’s Permissions

When you download the lender’s app, manage what information they access on your phone. Some will want access to your social media accounts, contact lists, call logs, and messages. With some lenders, it is not a must that you give them access to this date. They might still extend you the credit. Try to limit the app’s access to such information as much as you can.

4. Can You Afford the Loan

Most importantly, can you afford the loan? Don’t think about the principal amount only. What about the interest and other fees? Are you able to pay within the given period?

5. Stop Borrowing From Multiple Lenders

Sadly, most borrowers have multiple lending apps on their phones where they borrow from one lender to repay the other. That means you are relying highly on digital lenders.

Stop borrowing from any digital lender willing to give you money if you want to get out of debt. Of course, they are all willing to provide you with the money. It is business for them. For you, however, you are burying yourself in more debt.

6. Start Building an Emergency Fund

I’ve written numerous times that you need to have at least 6 months of living expenses in an emergency fund. Start building it slowly, even if you put Kes. 500 or 1,000 every month aside from your emergencies, it is still something. Whenever you come across a windfall (money you were not expecting), put it into repaying the debts you have and building an emergency fund.

That fund will save you from running into the arms of digital lenders when you need money to cover some emergency.

What’s your experience with digital lenders? Did you manage to get out of the debt?

DISCLOSURE: THE INFORMATION PROVIDED TO MY READERS IS GENUINE AND PRECISE TO THE BEST OF MY KNOWLEDGE. THE LINKS PROVIDED IN THIS ARTICLE DO NOT BELONG TO ANY AFFILIATE PARTNERS AND I AM NOT PAID FOR THEM. THE ARTICLE OFFERS GENERAL INFORMATION AND SHOULD NOT BE USED AS A SUBSTITUTE FOR PROFESSIONAL ADVICE OR HELP THAT CATERS TO YOUR INDIVIDUAL FINANCIAL GOALS. KINDLY SEEK HELP AND ADVICE FROM YOUR FINANCIAL ADVISOR FOR PERSONALISED ADVICE AND HELP. ANY ACTION TAKEN BASED ON THIS INFORMATION IS AT YOUR OWN RESPONSIBILITY AND RISK.

post a comment

You must be logged in to post a comment.