Retirement Planning: Why I am Counting On More Than My NSSF

Ihave been thinking about retirement lately. I might jump into the Financial Independence, Retire Early (FIRE) bandwagon. Maybe not. Whichever the case, I have been putting a lot of thought into how I would like my lifestyle to be during this period.

At the top of my list; probably retiring to a farm somewhere in the countryside where I can spend the rest of my golden years pretending to be a connoisseur of wines, brewing endless pots of coffee, and burying my head in books I have hoarded for years. Or travelling. This could work, too.

If you are getting ahead of yourself like me, here is a more important question, will your retirement savings be enough to afford your envisaged lifestyle? Perhaps this blast from the past might help in this regard. Basically, you need to save at least 80% of your present-day expenses for your retirement savings. Another more straightforward alternative is to multiply your monthly expenses by 12 to get the annual expenses. Then, multiply with 25 (a multiplier) to arrive at the amount you need to retire.

The above are just strategies to help you secure your retirement. Do not get a panic attack —like I did — when you see the figures. What you need could be lower or more based on several factors. Still, it is great to have a guiding estimate.

This brings me to saving for retirement, more specifically, NSSF savings. If you are in formal employment, your employer is mandated to deduct retirement contributions towards the national social security fund (NSSF). It should also include matching contributions from your employer.

I have not contributed to NSSF since I left corporate. But I have been thinking about returning to corporate and what my NSFF contributions would be when I finally retire. Would the payout be enough to fund my retirement if I relied only on this?

Probably not.

Why I am Counting On More Than My NSSF Contributions

I have seen that NSSF payouts are usually nothing to write home about. Imagine working for 30+ years and receiving a payout of fewer than 500,000 shillings. Unfortunately, this is the case for many senior citizens.

My mother went on early retirement a few months ago. She, of course, filed to withdraw her NSSF savings. I was not surprised by the amount she would receive, which was less than 300,000 shillings. Plus, having been in payroll accounting, I have seen statements of members following their issues and the payouts are not encouraging at all.

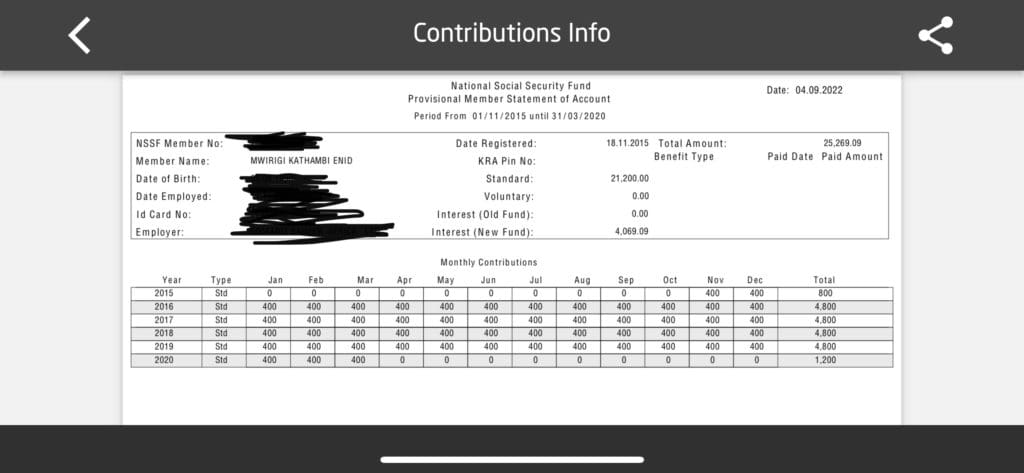

My own contributions statement notwithstanding. After months (possibly a year or so) of wondering how I could access my NSSF statement, I finally learned they had a working app a few days ago. I installed the app and can now view my statement. My total contributions for the 4 years and a few months I have been employed are 21,200 shillings. My total account balance, inclusive of returns, is 25,269.09. That brings my interest return to 4,069.09 shillings. Going by this trajectory and historical interest and payouts, I will likely receive less than 400,000 shillings. This amount is even lower if I do not contribute to NSSF anymore.

These calculations are based on NSSFs old rates. There is a pending law to increase the savings thresholds, which might help one increase benefits payout. Still, this amount might not be enough for many individuals.

The bottom line is that I am not counting on only my NSSF contributions to fund my retirement. So, I am looking and working towards some alternatives.

My Current NSSF Statement

More Ways to Comfort Proof Your Retirement

Securing a comfortable life will undoubtedly require more than NSSF savings. I believe it is also more than counting on retirement benefits from an employer. Having several options in place increases the chance of having the retirement lifestyle you are hoping to achieve. Below are some strategies you can incorporate:

Start by Increasing Your NSSF Contributions

Yes, you can contribute more than the minimum required amount. All you have to do is request your employer to top up your contributions with whatever amount you are comfortable adding to your monthly contributions.

Increasing your contributions allows you to set more money aside, thus earning more interest. It also helps you reduce your tax liability for the year. Remember that your pension contributions are tax-deductible for up to 20,000 shillings.

Increase Your Contributions to Your Employer’s Scheme

You can also contribute more than your base contribution if you are lucky enough to have an employer with a pension or provident scheme. These schemes are usually run by a third-party institution. As such, most are more likely to have higher returns than NSSF. Your employer might not match your contribution past their set base. Still, your extra contribution will grow your kitty while providing you with tax benefits.

Get a Personal Pension or Provident Fund

A second option, and one I would recommend more, is to have a personal pension or provident fund. You could automate contributions to this account, do it manually or ask your employer to deduct the money from your salary and remit it to your fund account. With the last option, keep track of your account to ensure the contributions are remitted.

Why am I recommending this? First, most firms offering these plans have a higher interest return than NSSF. Second, if your employer/s have a pension scheme, you can always consolidate your contributions here anytime you change camp. Third, you have absolute control over the account. Finally, you can always move to another provider without seeking approvals from fund managers, like it is with employer schemes.

Investing More in Income Generating Assets

The goal here is to have assets that generate passive income. These include shares, REITs and real estate. If you bought these assets when young, you would also enjoy benefits from capital appreciation. Bonds are also an excellent strategy. If you can match a few bonds with your retirement, you will receive a lump sum payout of your investment. This money can go towards funding various retirement expenses.

Related post: Individual Retirement Plans vs. Life Insurance Policy; What You Need to Know

Building or Buying a House

I believe most of us would love to stop paying rent finally. But building or buying a house is a cash-intensive project. Fortunately, it is not something you need to do in a month or two. Some people build their homes in a few months, which you can do if you have the money. Others build over time, having milestones for each house section depending on the available cash. A mortgage is another alternative to owning a home. Instead of a mortgage, you can also get a normal loan, which is usually cheaper than a mortgage. Did you know that you can use 60% of your pension savings as collateral for the money you borrow to build a home? What method suits you?

If you can, plan to have a retirement home before your retirement date. That way, your pension payouts will not go towards this project, as it would wipe a considerable chunk of your payout.

Final Thought

I believe one’s current lifestyle, financial situation and goals can help determine where you might stand when it is time to retire.

For instance, let’s say you already have a house, a farm, or investments in assets like company shares and government bonds. Going by this, we can assume you do not have to worry about rent payments. However, if you plan to relocate to the upcountry upon retirement, your worry will be the maintenance costs for your house, which might not be as high as rent payments. Your farm would also provide foodstuffs, reducing food costs and possibly serving as an additional cash flow if you sell your farm produce.

In addition, your investments in shares, government bonds and other assets will provide you with passive income from interest and dividend payments. Or you can also sell to recover your capital and possibly make a profit while at it.

With some of these strategies in place, you can expect a handsome payout from your NSSF, employer or personal pension contributions. Or, you will have invested your money in assets that continue to generate passive income to fund your lifestyle in your golden years.

I am working on increasing my payout from my personal provident plan, generating passive income and having a farmhouse. What’s your plan?

Eric

Great content. Definitely betting on catching up with all the movies I can’t watch now. It would be interesting to see how protected pension schemes are. Kenya has a little history of institutions going under. The percentage of protected contributions (deposits for banks) hasn’t helped build any confidence. Perhaps that’s why what I would describe as the traditional route to retirement planning – . pension funds – has not really taken off beyond employer schemes and for ‘p&p’ civil servants.

Enid Kathambi

Very true. Then there are limited financial literacy programs for these products and how they can help in retirement planning.

John

Good analysis . Keep it up

Enid Kathambi

Thank you, John.