Are Education Insurance Plans Worth It?

Are education insurance plans worth it? With the high cost of education and the ever-increasing costs, who wouldn’t want to plan for their child’s future education? I know I would.

But are education insurance plans worth it? NOT AT ALL! Yes, it will give you that consolation an insurance product provides of knowing that you are covered if the insured risk occurs. And, if you are not a consistent saver, you are forced to pay your premiums on time lest you lose everything.

That said, education insurance policies are more than an insurance product. These come with the component of saving and investing.

And you know the number one rule of investing and risk management, NEVER MIX THE TWO!

Education Insurance Plans in Kenya: Are They Worth It?

While you want your child to have the best education possible, think twice before purchasing an education insurance plan.

The premiums for these policies are pretty enticing and low, with other rider benefits should you die, get sick or be disabled. Not forgetting the saving and investment component, where your premiums are invested in fixed assets, equities or a balanced fund by the institution.

And for this reason, I would say that education insurance plans are not worth it. Why? For the same reason why experts recommend against taking an endowment life policy.

Insurance products are just that: risk management products to cushion you if any risks, like sickness, fire, accidents or death, occur. This is where health, auto, home, and whole or term insurance covers come in. They are pure insurance products, with no other complementary products serving as a saving or investment vehicle.

Is your concern saving and investing for your child’s future? In that case, you are better off putting that money in a high-yield savings account or buying any investment asset. The best way to go about this is to start saving and investing at an early age. Do not wait to start saving for their college when they are in high school already. If you can, it’s best to start building that savings or investment fund for their education when they are younger, even after birth. If you work with a financial planner or advisor, they can even help you get investment assets that match specific stages of your kid’s education.

Let’s Do The Math: Education Insurance Plans vs Pure Investment Assets

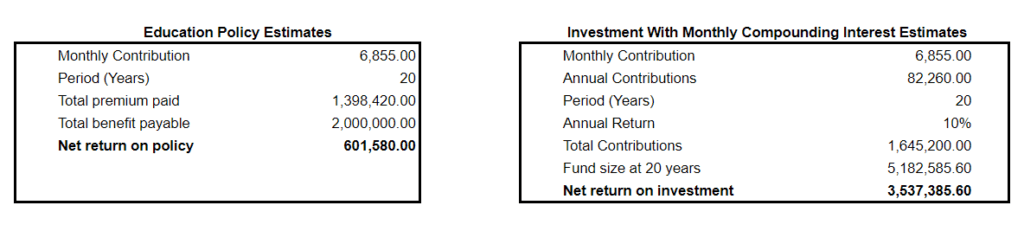

Let’s take an example. As I was researching, I came across an education plan offered for 20 years. The monthly and total premiums are around Kes. 6,800 and Kes. 1.39M with an indicative benefit payout of Kes. 2M. This will earn you a return of about 600,000 after 20 years.

If you were to invest on your own, say, the same monthly premium at an annual return of 10%. Depending on a few factors, you will have a fund size of between 4.5M to 5.2M compared to the Kes. 2M insurance payout.

I have used several online calculators to simulate these figures, and the differences in the total return are telling (see the below example). If you invest on your own, you make a return that’s way higher than what the insurance policy is offering, even with those bonuses and tax relief that it offers!

But what if I lose my job, pass on, become bedridden or disabled? What happens to my child’s future? Unfortunately, these are the fears brokers will sell when they want you to buy an education policy. But remember what we said? Never let emotions rule your investment decision.

Yes, most insurance providers promise you that if such misfortunes befall you, the premiums will stop, and your child will receive the cash payout at maturity. There is also the promise of getting some payouts a few years before maturity. Quite enticing!

The return is still lower than a pure investment product offers, even a simple Money Market Fund. Better still, lock that money in a credible Sacco.

Education Insurance Plans vs. Life Insurance

Are you worried about your child’s future when you are not there or are incapacitated? How about you leverage that investment product with a pure insurance cover, like a whole-life or term-life policy? Again, notice that I have left out an endowment life policy here? Because It’s another insurance product with an investment component, and it’s not worth it.

There is a high possibility that the payout from a life insurance cover will be higher. You might also get lower premiums because insurance products with an investment component always charge a higher premium.

While education insurance plans provide tax relief, this benefit doesn’t seem like a price to pay for such a steep difference in the total return of the two products. In Kenya, these insurance policies get you a tax deduction of 15% on the premium paid, with a cap of Kes. 5,000 per month (Kes. 60,000 per year). You can get the same tax relief with a life insurance policy!

Also, an investment product provides you with more flexibility when it comes to withdrawing. With certain protections, you can get your capital back. On the other hand, if you stop paying your insurance premiums, you will lose everything. And, if you were to cancel the policy, you will only receive a surrender value after a certain period, usually lower than your payout and total paid out premiums.

The bottom line is to avoid insurance products masquerading as saving and investment avenues. It doesn’t matter whether it is an education insurance plan or a life insurance policy. If you want to protect yourself against risks, just buy a pure insurance product. Get a whole life or term life insurance policy. But, if you want to save and invest for whatever goal, invest in bonds, stocks, mutual funds, and real assets.

Benard

How about funeral covers?

Enid Kathambi

While planning for your funeral expenses is a good idea and will save your family some money and all funeral planning stress. However, some of these funeral insurance covers might be more expensive than you would actually need for funeral expenses. You can try estimating how much you might need to meet such expenses, and compare with how much you have to pay in premiums. Also, consider whether the premiums increase over the years, as some get more expensive as you age. Also, some have a waiting period, meaning your beneficiaries will not receive any payout if you die within this period. A great alternative is to get a whole life insurance cover. The money might not be immediately available for funeral expenses but it will be a more significant amount for their future expenses.